Debanked? How to still accept payments

If you have been debanked, you can keep accepting payments by moving on two tracks at once: recover what you can from the old provider, and stand up a payment method that cannot be cut off again. The fastest cut-off-proof option is a non-custodial crypto gateway that settles straight to a wallet you control — there is no account for anyone to close and no balance for anyone to freeze. This guide covers the first 48 hours, your replacement options compared, and how to make the fix permanent.

First: stabilize, do not panic

Getting debanked feels like the floor dropped out — payouts stopped, maybe a balance frozen, and a support team that will not explain. It is survivable. The merchants who recover fastest do not waste days arguing; they secure what they can and immediately set up an alternative rail so revenue does not stop.

What to do in the first 48 hours

- Screenshot everything — the notice, your balance, any held funds, every message. It is your record if you dispute or complain.

- Move any accessible cash out to a separate institution before more of it gets frozen.

- Ask for the reason in writing. You may not get a straight answer, but the paper trail matters.

- Warn the people who depend on payouts — staff, suppliers — before a missed payment surprises them.

- Redirect new sales now. Get a payment link live so the next order does not bounce.

Your replacement options, honestly compared

| Option | Speed to normal | Risk of being dropped again | Who holds the money |

|---|---|---|---|

| Another bank or EMI | Fast | High — same risk model that just dropped you | The bank (custodial) |

| High-risk payment specialist | Slow onboarding | Medium, but with high fees and rolling reserves | The processor (custodial) |

| Non-custodial crypto | Under an hour | None — no account to close | You, in your own wallet |

Another bank or EMI is the fastest to feel normal, but you are re-exposed to the same risk model — especially if your category was the reason. A high-risk specialist is built for flagged industries, but the trade-off is higher fees, rolling reserves, and slow onboarding, and it is still custodial. Non-custodial crypto is the only option where no provider holds your money at all.

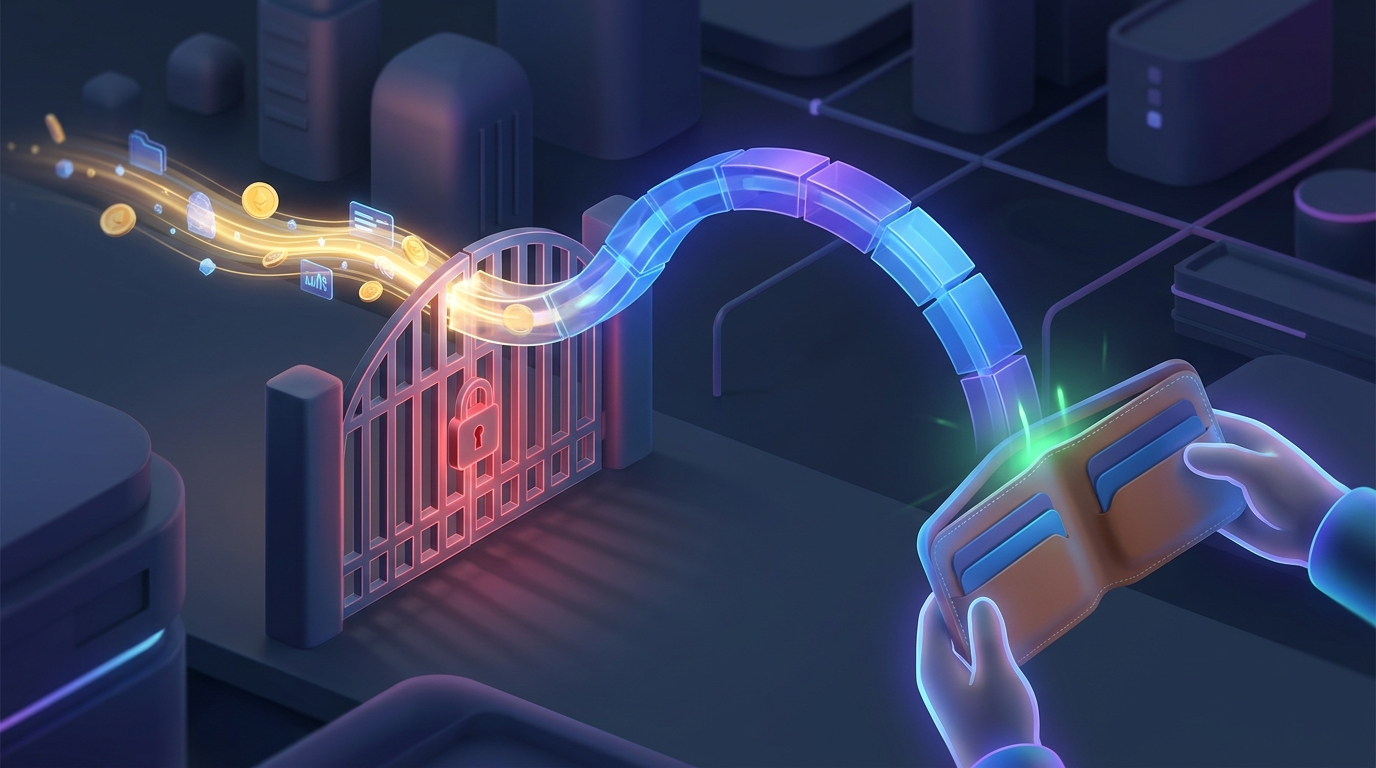

Why crypto is the un-debankable rail

With CryptoGate, you connect your own wallet and customers pay you directly. We never custody funds, so there is no balance to freeze, no payout to withhold, and no KYC gate to fail. It is the same structural fix that protects against a frozen Stripe account or a 180-day PayPal hold — the money simply never passes through a third party that can stop it. See exactly how crypto protects against debanking for the mechanics.

You can be live in well under an hour with a payment link, a hosted checkout page, or the API, accepting Bitcoin, Ethereum, Litecoin, Dogecoin, Dash, and stablecoins like USDT and USDC. If you sell online, drop it into a Shopify store or WooCommerce checkout.

Make it permanent

The merchants who recover fastest from debanking treat it as a lesson, not a one-off: they keep a non-custodial rail running permanently so a single provider can never again decide whether they get paid. For the wider context, see what debanking is and which industries are most at risk. When you are ready, start free with CryptoGate.

Frequently Asked Questions

What does it mean to be debanked?

Being debanked means a bank, card processor, or payment provider has terminated its relationship with you — closing your account, freezing your balance, or refusing service — usually with little warning and no detailed explanation, even though your business is legal.

How can I still accept payments after being debanked?

Set up a payment rail that does not depend on a bank account. A non-custodial crypto gateway like CryptoGate lets customers pay straight to a wallet you control, so there is nothing for a provider to close or freeze. You can be live in under an hour with a payment link or hosted checkout.

Will another bank just debank me again?

It can, if your category was the reason. Opening an account at a similar bank or EMI re-exposes you to the same risk model. That is why many debanked merchants pair a new account with a non-custodial rail that has no account to close, so revenue keeps flowing even if the bank changes its mind.

Do I need KYC to accept crypto payments after being debanked?

Not with a non-custodial gateway. Because CryptoGate never holds your funds, there is no custodial obligation that would require identity verification to onboard. You still handle your own taxes and business compliance as the owner.

Can I keep my bank and add crypto as a backup?

Yes, and most merchants do exactly that. They run cards and banking for the customers who prefer them and add a non-custodial crypto rail alongside as insurance, so if they are ever cut off again, payments continue uninterrupted.